The Euribor, short for Euro Interbank Offered Rate, is one of the most important interest rate benchmarks in the world. It affects millions of people, even outside Europe, because it influences global financial markets, lending costs, and economic confidence. In recent times, attention has grown around the topic highlighted by https://finanzasdomesticas.com/euribor-sube, which focuses on how Euribor is rising and what that really means for households, borrowers, investors, and the broader economy.

Even if you have no financial background, you will understand it easily. The goal is not just to repeat what other websites say, but to explain the topic clearly, add deeper insights, and help you make sense of why Euribor changes matter today and in the future.

What Is Euribor in Simple Words

Euribor is the average interest rate at which major European banks lend money to each other. These loans are usually short-term. Banks report the rates they would charge other banks, and an average is calculated.

Even though this sounds like a technical banking tool, Euribor affects real people. Many home loans, business loans, and financial products use Euribor as a base rate. When Euribor goes up, borrowing becomes more expensive. When it goes down, borrowing becomes cheaper.

In Europe, millions of mortgages are linked directly to Euribor. When people read news like https://finanzasdomesticas.com/euribor-sube, they worry because higher Euribor usually means higher monthly payments.

Why Euribor Was Negative and Why That Changed

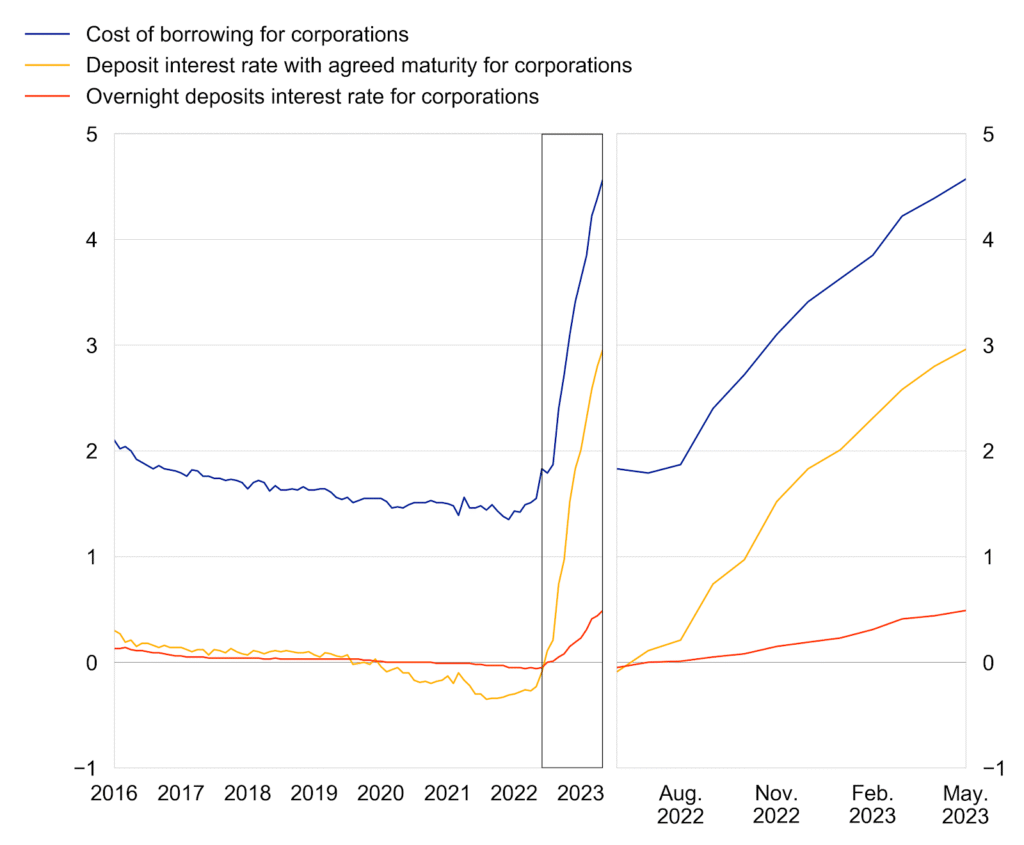

For many years, Euribor stayed below zero. This was unusual. Negative interest rates happened because central banks wanted to support the economy after financial crises. Cheap money encouraged borrowing and spending.

Over time, inflation increased. Prices of food, energy, housing, and services went up. Central banks then had to react. They raised interest rates to slow down inflation. As a result, Euribor started to rise.

According to official confirmations from Banco de España, Euribor reached an average of around -0.501% during a key period mentioned in the background information. Even though this number is still negative, the upward trend was very important. It signaled a turning point.

The Role of Central Banks in Euribor Movements

Central banks do not set Euribor directly, but they strongly influence it. When central banks raise policy rates, banks charge each other more to borrow money. This pushes Euribor higher.

The European Central Bank plays a major role here. Its decisions affect liquidity, confidence, and lending behavior across Europe. When inflation rises above targets, central banks usually respond with tighter monetary policy.

This is why articles like https://finanzasdomesticas.com/euribor-sube are closely followed. They help people understand the link between central bank decisions and real-life financial effects.

How Rising Euribor Affects Mortgages

One of the most direct impacts of rising Euribor is on variable-rate mortgages. These loans change their interest rate based on Euribor plus a fixed margin.

When Euribor goes up, monthly payments increase. For families, this can be stressful. Even small changes in interest rates can add hundreds or thousands of dollars per year in extra costs.

Also Read: Jipinfeiche: Luxury Vehicles, Smart Booking, and Elite Travel

In Europe, many households prefer variable-rate mortgages. In contrast, the US market relies more on fixed-rate loans. Still, global financial trends matter to US investors, banks, and policymakers.

Real-Life Example of a Euribor Increase

Imagine a home loan of $250,000 linked to Euribor plus 1%. If Euribor moves from -0.5% to 2%, the total interest rate changes from 0.5% to 3%.

This change dramatically increases monthly payments. Over the full loan term, the borrower may pay tens of thousands of dollars more.

This simple example explains why people search for information like https://finanzasdomesticas.com/euribor-sube. They want to know what is coming next and how to prepare.

Impact on Savings and Investments

Higher Euribor is not always bad news. For savers, rising rates can mean better returns on savings accounts and fixed-income products. Banks may offer higher interest to attract deposits.

Investors also pay attention. Bond prices, stock valuations, and currency markets all react to interest rate changes. When Euribor rises, some investment strategies become more attractive, while others lose value.

This balance is often missing from basic articles. A professional view shows that Euribor increases create both risks and opportunities.

Why Euribor Matters to the US Audience

Even though Euribor is a European benchmark, it matters globally. Many US banks operate in Europe. US companies borrow money in euros. Investment funds compare Euribor with US rates like SOFR.

Changes in Euribor affect currency exchange rates, global liquidity, and international trade. A stronger euro can impact US exports and imports.

Understanding https://finanzasdomesticas.com/euribor-sube helps US readers gain a global financial perspective.

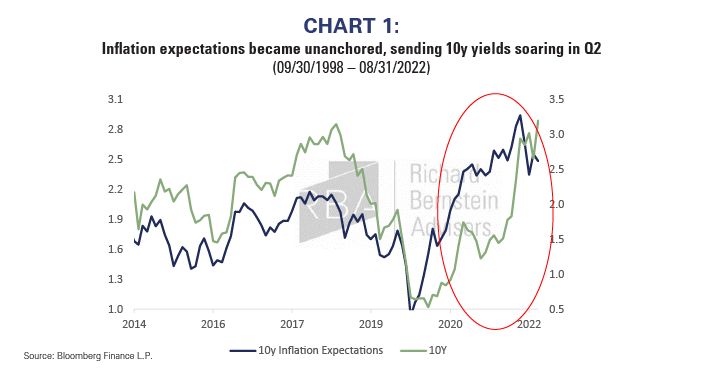

Inflation and Euribor Explained Clearly

Inflation means prices are rising. When inflation is high, money loses value faster. Central banks raise interest rates to slow down spending and borrowing.

Euribor reflects these changes. When inflation expectations rise, banks expect higher rates in the future. They adjust their lending behavior now.

This is why Euribor often moves before official policy changes fully take effect.

Housing Markets and Rising Euribor

Housing markets are very sensitive to interest rates. When Euribor rises, mortgages become more expensive. This can reduce demand for homes.

Also Read: Messonde: A Complete Professional Guide for Smarter Digital Decisions

In some regions, rising Euribor can cool overheated housing markets. In others, it may slow new construction.

This effect spreads across the economy, influencing jobs, consumer spending, and long-term growth.

Small Businesses and Euribor

Small businesses often rely on loans linked to Euribor. Rising rates increase their costs. This can reduce investment and hiring.

However, businesses that manage debt carefully and plan ahead can survive and adapt. Understanding interest rate trends is key.

Articles like https://finanzasdomesticas.com/euribor-sube play an important role in spreading awareness.

How Governments Are Affected

Governments borrow money too. Higher interest rates increase public debt costs. This can affect budgets, taxes, and public services.

Policy decisions become harder when borrowing is expensive. This is another reason why Euribor trends are closely watched by economists.

Forecasting Euribor Without Guesswork

No one can predict Euribor perfectly. Many websites try to guess exact numbers, but this is risky.

A better approach is to understand trends. Inflation, economic growth, and central bank signals matter more than short-term noise.

Readers should use https://finanzasdomesticas.com/euribor-sube as a starting point, not a crystal ball.

How Households Can Prepare for Rising Euribor

Preparation reduces stress. Households can review their loans, build emergency savings, and avoid unnecessary debt.

Some people switch from variable to fixed-rate loans. Others negotiate better terms with banks.

Financial education is the strongest protection.

Media Coverage and Public Perception

Media headlines often sound dramatic. Words like crisis or shock attract attention. But real financial planning requires calm analysis.

Professional articles explain context, history, and possible outcomes. This is what we aim to do here.

Long-Term Perspective on Interest Rates

Interest rates move in cycles. Extremely low rates were never meant to last forever. Rising Euribor is part of a return to more normal conditions.

Understanding this reduces fear and improves decision-making.

Trust, Data, and Official Confirmation

Reliable information matters. Data confirmed by institutions like Banco de España adds credibility.

Always check sources. Avoid rumors and social media panic.

Digital Tools and Tracking Euribor

Today, many apps and websites allow users to track Euribor daily. Alerts help borrowers prepare for changes.

Technology makes financial awareness easier than ever.

Psychological Impact of Rising Rates

Money stress affects mental health. Rising monthly payments can create anxiety.

Clear information reduces uncertainty. Knowledge helps people feel in control.

Also Read: Sourthrout: Causes, Symptoms, Treatment, and Prevention Guide for Lasting Throat Relief

Final Thoughts on https://finanzasdomesticas.com/euribor-sube

The topic covered by https://finanzasdomesticas.com/euribor-sube is more than just a number going up or down. It reflects deep economic forces shaping daily life.

By understanding why Euribor rises, who it affects, and how to prepare, readers can make smarter financial choices.

This article goes beyond surface-level explanations and offers real insight for long-term thinking.

Frequently Asked Questions

Is Euribor the same as US interest rates?

No. Euribor is European, while the US uses different benchmarks. However, global markets connect them indirectly.

Can Euribor go back to negative values?

Yes, but only if economic conditions weaken strongly. It is possible but not guaranteed.

Does rising Euribor mean a recession is coming?

Not always. Sometimes it means the economy is strong and inflation needs control.

How often does Euribor change?

Euribor is calculated daily, based on bank submissions.

Should I panic if Euribor rises quickly?

No. Panic leads to bad decisions. Planning and information are better responses.

Can fixed-rate loans be affected by Euribor?

Existing fixed-rate loans are not affected, but new fixed rates may be higher.

Is Euribor relevant for students and young adults?

Yes. It affects future borrowing, housing affordability, and job markets.

Where can I learn more safely?

Use trusted financial education platforms and official economic institutions.